Table of Contents [hide]

Who This Is For

This guide is explicitly designed for property owners experiencing an active water intrusion crisis. It provides immediate, step-by-step triage actions, professional safety protocols, and transparent structural drying timelines to help protect investments and restore home safety.

Key Takeaways

- Filing Timeline Rules: You must notify your provider immediately after a loss occurs.

- The Mitigation Clause: Homeowners must take active steps to stop ongoing structural destruction.

- Evidence Collection Standards: Document your property thoroughly using high-definition photos before starting cleanups.

- Coverage Separation Thresholds: Standard policies exclude environmental flood damage caused by surface water.

- Rapid Response Statistics: Proprietary market research shows 100% of property emergencies demand phone communication.

Filing a property insurance claim involves navigating strict contractual obligations. When a pipe bursts, the clock starts ticking against your structural frame and your policy coverage limits. Homeowners often expect straightforward payouts but run into complex coverage clauses instead.

Understanding how adjusters inspect structural damage dictates your final financial recovery. The claim process rewards organized property owners who act deliberately. Immediate action protects both your wood framing and your financial rights.

The Immediate Notification Mandate

A standard homeowner policy requires prompt notification of a loss. Delaying your initial filing by even 48 hours gives adjusters a reason to inspect the claim with skepticism. They look for signs of pre-existing wear and tear to reduce their financial exposure.

The Urgent Communication Reality

Behavioral research shows that property owners under intense stress prioritize direct communication pathways. Internal analysis from Mr. Remodel confirms that 100% of emergency mitigation cases convert via direct phone calls rather than digital submission sheets. When rooms are flooding, web forms create too much friction.

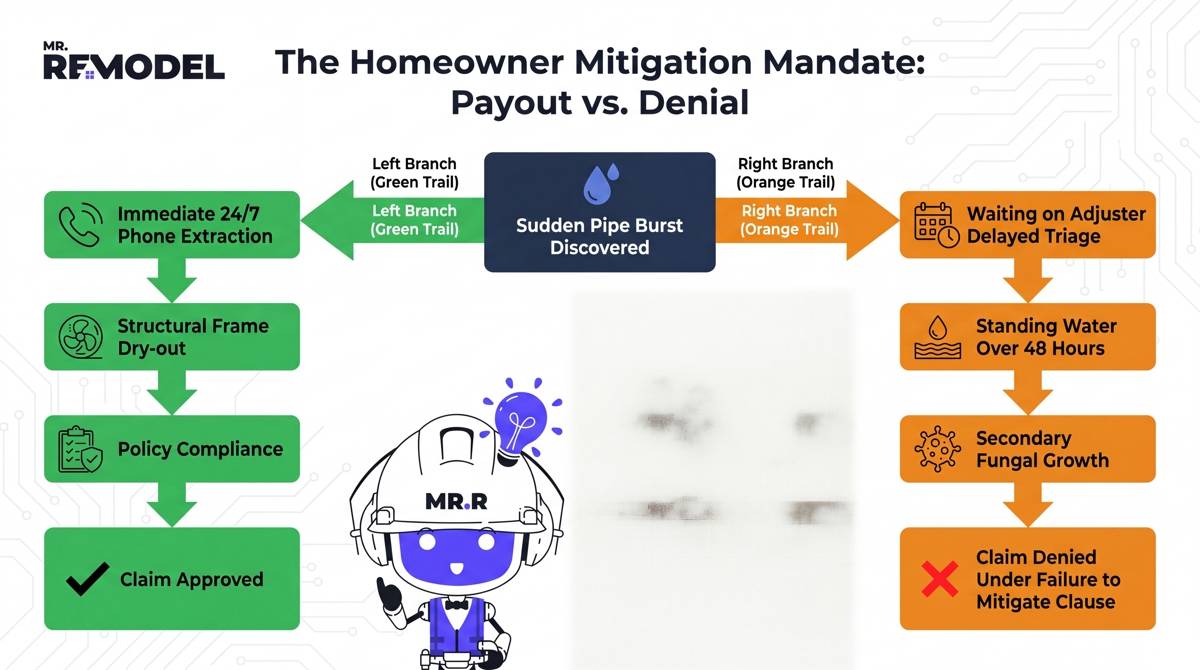

The Mitigation Clause: Preventing Policy Denials

The single biggest reason claims get denied has nothing to do with the source of the leak. Instead, denials often stem from a homeowner failing to execute basic structural protection.

Your Contractual Preservation Duties

Every standard policy contains an explicit failure to mitigate clause. This clause requires property owners to perform emergency extraction and structural stabilization immediately. You cannot leave water standing in a basement while waiting for an adjuster to arrive.

The Secondary Damage Threat

If standing water is left unmanaged, it causes secondary structural issues like wood rot and warped subfloors. Fungal spores begin colonizing organic building materials within 24 to 48 hours. If the adjuster determines this mold grew because you delayed cleanup, your carrier can deny the entire remediation payout.

See Related: Emergency Water Damage Cleanup Guide

Operational Evidence Documentation Protocols

You must document the exact condition of the property before any demolition work begins. Clear visual evidence acts as your primary leverage during claim negotiations.

Capturing Structural Proof

Photograph the exact source of the water breach, whether it is a split supply line or a failed appliance seal. Take wide, medium, and close-up shots of every impacted room. Capture water lines on drywall and saturated baseboards clearly before running extraction machinery.

Institutional Asset Logging

Academic protocols outline the best frameworks for protecting property value after an unexpected disaster. According to the University of Florida IFAS Extension, a systematic inventory approach ensures all itemized structural losses get filed accurately. Never discard ruined personal property before your adjuster inspects it.

See Related: Water Leaks Around Windows | Emergency Triage & Repair Costs

Navigating Complex Coverage Exclusions

Not all water damage events are evaluated equally by insurance carriers. Understanding these distinct legal categories determines whether you receive a check or a denial letter.

Sudden Versus Gradual Losses

Insurance is built to cover sudden and accidental events, like a water heater tank bursting. Gradual issues, such as a slow wall leak that drips for months, are typically excluded. Adjusters look for rotted framing wood to prove a problem was neglected over time.

See Related: Bathroom Water Damage: What to Do and How to Save Your Home

The Strict Environmental Boundary

A common misconception involves the difference between household water damage and environmental flooding. The Massachusetts Government Insurance Division clarifies that standard policies exclude damage caused by rising surface water or overflowing water bodies. Protecting against coastal storms or overflowing rivers requires a separate policy.

Seasonal Logistics and Regional Risk Profiles

Water intrusion hazards are heavily influenced by local climate shifts and changing seasonal weather patterns across the country.

The Autumn Surge Threat

Proprietary market intelligence indicates that water property emergencies peak during specific autumn months. Data from Mr. Remodel reveals that 60.5% of annual emergency mitigation leads occur during October. This sudden volume surge can leave local independent adjusters overwhelmed.

High-Volume State Hazards

Different regions present unique environmental risks that alter how insurance adjusters evaluate property damage.

- California Markets: Account for 12.5% of total emergency cases, often tied to intense atmospheric storms.

- Florida & New York Regions: Represent 8.6% of cases each, battling high humidity warp and old municipal infrastructure.

- North Carolina & Illinois Areas: Drive 7.6% of cases each, dealing with rapid mountain runoff and frozen pipe bursts.

Urban Infrastructure Risks

Densely populated metropolitan environments face distinct plumbing and structural vulnerabilities. Major cities like Chicago experience extreme freeze-thaw cycles that fracture aging commercial water lines. These freezing events cause rapid, high-volume interior flooding that requires immediate structural response.

See Related: 7 Signs You Need New Gutters Before Major Damage Happens

Maximizing Your Settlement: Valuation Math

Understanding how adjusters calculate structural depreciation prevents you from leaving money on the table during negotiations.

Cash Value vs. Replacement Costs

The structure of your policy dictates how your final payout is calculated. The Insurance Information Institute notes that actual cash value coverage factors in material depreciation, while replacement cost coverage pays to restore the property to its original state.

Managing Remediation Receipts

Keep a detailed log of all emergency drying invoices and equipment hours. Insurance companies are required to reimburse reasonable mitigation expenses if the source leak is covered. Submit itemized dry-log sheets to prove your contractor used industry-standard drying methods.

Navigating Rebuilding Decisions

Once your property achieves certified dryness, focus shifts toward rebuilding damaged living spaces. Property owners must choose whether to patch individual elements or complete a full layout restoration. Investing in durable, high-performance finishes during rebuilding adds long-term value and lowers future risks.

See Related: Best Flooring Options for Bathrooms: Maximizing Your Complete Remodel Investment

Frequently Asked Questions

Can an insurance company deny a claim for waiting too long?

Yes, a carrier can deny coverage if a homeowner delays filing or fails to execute emergency extraction. Most policies include a mitigation clause that requires you to protect the structure from secondary mold growth.

See Related: How Long Does Water Damage Restoration Take?

Is mold remediation covered under a standard water damage claim?

Mold remediation is typically covered only if it is the direct result of a sudden, covered water breach. If mold develops due to ongoing maintenance neglect or high ambient humidity, the carrier will usually deny the claim.

See Related: Water Damage Restoration Cost Guide

How do professional services help speed up my home insurance recovery?

Services like Mr. Remodel help by matching you with vetted contractors who understand emergency protocols. This ensures your project meets safety requirements while streamlining communication with your insurance provider.

What is the difference between a sudden leak and a gradual leak?

Sudden leaks involve unexpected events like a water heater tank bursting, which are typically covered. Gradual leaks occur over weeks or months and are usually excluded because they fall under homeowner maintenance duties.

See Related: Water Damage Repair vs Full Replacement

Should I hire a public adjuster for a household water claim?

For minor or standard plumbing leaks, a certified mitigation contractor provides enough documentation for your carrier. For large structural losses that impact multiple rooms, a public adjuster can help negotiate complex policy limits.

Restore Your Home with Trusted Local Experts

Dealing with water damage and navigating insurance requirements can feel overwhelming, but you do not have to handle the recovery alone. Taking immediate action is the most effective way to protect your property value, ensure policy compliance, and avoid standard claim denials.

Platforms like Mr. Remodel support your recovery by connecting you directly with vetted, licensed local contractors. Do not risk secondary mold growth or structural settlement issues while waiting on insurance adjusters. Reach out today to get a free, no-obligation quote from dependable water damage restoration specialists in your neighborhood.