Table of Contents [hide]

Who This Is For

This guide is written for homeowners who have experienced a recent severe weather event (hail, high winds, hurricane, or heavy snow) and need an actionable, step-by-step system to visually document roof damage, file an airtight insurance claim, and avoid underpayment or claim denial.

Key Takeaways

- High-Stakes Claims: Data from Mr. Remodel reveals that the average full roof replacement claim across thousands of analyzed projects stands at $25,307, with major storm replacements reaching up to $57,146. Proper documentation directly protects this substantial financial recovery.

- Replacement vs. Repair: 99% of storm damage leads require full roof replacement rather than minor spot repairs because structural integrity is compromised across entire slopes.

- Time-Sensitive Action: In major storm corridors, 16.6% of affected homeowners require emergency response within 24 hours to prevent interior water damage and mold growth.

- Systematic Evidence: Documenting hail strikes, lifted shingles, damaged attic decking, and soft metal impacts creates an undeniable paper trail for your insurance adjuster.

When a severe hail storm or high-wind event passes over your neighborhood, the damage to your roof isn't always immediately obvious from the ground. However, even minor leaks or missing shingles can compromise your home's structural integrity over time.

Filing a successful insurance claim depends on thorough, organized documentation. Insurance adjusters require clear, visual proof that links the physical damage on your roof directly to the specific storm event. Skipping systematic documentation steps often leads to delayed processing, partial approvals, or outright claim denials.

The Financial Stakes of Storm Damage Documentation

A storm-damaged roof is far more than a cosmetic concern. According to data tracked across 17,097 project leads by Mr. Remodel, the national average sale value for a full roof replacement is $25,307, with severe storm restorations reaching as high as $57,146.

Furthermore, analysis shows that 99% of storm damage inquiries require a full roof replacement rather than localized patching. When high winds tear off shingle tabs or hail fractures the underlying fiberglass matting, the protective integrity of the entire roofing system is compromised. Thorough documentation ensures your insurance carrier approves a complete system replacement rather than an inadequate spot repair.

See Related: Storm Damage: Repair or Replace Decision Guide

Step-by-Step Roof Damage Documentation Checklist

To build a strong claim, you must document damage across four key areas: ground-level surroundings, soft metals, primary roofing materials, and interior spaces.

Step 1: Establish the Event Timeline

Before stepping outside, document the exact date and approximate time the weather event occurred. Download local meteorological reports or news bulletins confirming hail size (e.g., 1.5-inch diameter) or peak wind gusts (e.g., 60+ mph) in your zip code. Insurance carriers require a specific date of loss to process your file.

Step 2: Conduct a Ground-Level Perimeter Audit

Begin your visual documentation at ground level. Safety is paramount—never walk on a wet or structurally compromised roof. Take wide-angle photos of your entire house, then take close-up photos of collateral damage:

- Siding & Trim: Look for dented aluminum siding, cracked vinyl panels, or chipped exterior paint.

- Window Screens & Frames: Dented window frames and torn screens serve as clear evidence of directional hail or flying debris.

- Patio Furniture & Fencing: Document dented metal furniture, shattered skylight covers, or broken fence panels.

Step 3: Inspect "Soft Metals" for Hail Collateral

Soft metals on your roof and exterior retain dent marks more clearly than asphalt shingles. Insurance adjusters inspect these components first to verify hail impact density:

- Gutters and Downspouts: Take close-up photos of dent marks on seamless aluminum gutters and downspouts.

- Roof Vents and Flashing: Document dings on metal ridge vents, turtle vents, pipe boots, and chimney flashing.

Step 4: Document Primary Shingle and Roof Surface Damage

If accessing the roof safely via a ladder (or through a professional inspector):

- Hail Impacts: Look for dark, circular bruising where granules have been knocked away, exposing the dark asphalt substrate underneath. Touch the bruised spot—if it feels soft or spongy (like an apple bruise), the underlying mat is fractured.

- Wind Damage: Photograph creased, flipped, or missing shingle tabs. Wind damage often manifests as clean horizontal tear lines near the sealant strip.

- Granule Loss in Gutters: Check the bottom of your downspouts. Heavy accumulations of loose granules signal accelerated shingle deterioration.

See Related: Roof Replacement Cost by Material (Asphalt, Metal, Tile, Slate)

Step 5: Perform an Interior Attic and Ceiling Audit

Storm damage often penetrates deep into structural framing before dripping through living room ceilings. Head into your attic with a flashlight:

- Inspect the underside of the plywood roof decking for dark water stains, active drips, or damp insulation.

- Take clear photos of any ceiling water rings or bubbling drywall paint in upper-floor rooms.

Navigating the Adjuster Meeting with Concrete Proof

When your insurance carrier assigns an adjuster to inspect your property, having an organized documentation binder (or digital photo folder) changes the dynamic from a subjective guess to an evidence-based discussion.

Organizational Standards for Photo Evidence

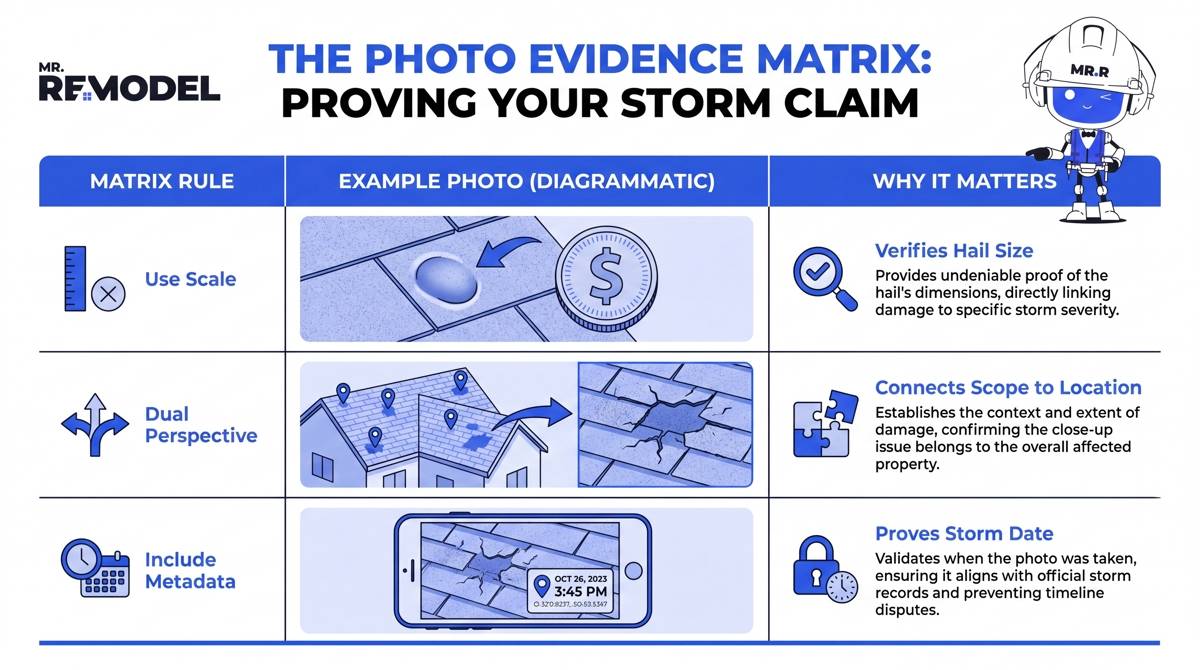

- Use Time & Date Stamps: Ensure your digital camera or smartphone records precise metadata for every photograph.

- Include Scale References: Place a tape measure or coin next to hail dents on soft metals or shingle bruises to clearly show impact dimensions.

- Take Dual-Perspective Shots: Capture one wide-angle photo showing the entire roof slope, followed immediately by a close-up photo of the specific damage on that same slope.

Formal inspection protocols, such as those outlined by the National Residential Code & Inspection Association (NRCIA), emphasize defining a "test square" (a 10ft x 10ft area) on each roof slope. If an adjuster counts more than 8 to 10 distinct hail hits per test square, the entire slope generally qualifies for full replacement under standard underwriting guidelines.

See Related: Insurance Claims vs Out-of-Pocket Roof Replacement

Post-Claim Upgrades and Material Decisions

Once your insurance claim is approved, you have an opportunity to select replacement materials that provide better defense against future storms. Data shows that 67.5% of homeowners choose architectural asphalt shingles due to their balance of cost and durability, while 17.9% upgrade to standing-seam or ribbed metal roofing systems for maximum impact resistance.

Upgrading to Class 4 impact-resistant shingles or metal roofing during a claim-funded replacement can also qualify you for annual homeowner insurance premium discounts of 5% to 20%, depending on your state and carrier.

See Related: Roof Replacement Cost (2026): Materials, Labor, Regional Pricing & ROI

Professional Inspection vs. DIY Safety Limits

While ground-level documentation can be safely completed by any homeowner, accessing a storm-damaged roof carries severe safety risks. Loose shingles, wet moss, structural deck soft spots, and steep pitches contribute to thousands of residential ladder injuries each year.

State disaster guidelines, such as those issued by the Tennessee Department of Commerce and Insurance (TDCI) and municipal building authorities like the City of Boulder Roof Inspection Division, strongly advise homeowners to hire licensed, bonded, and insured contractors for physical roof-top inspections.

When you need a professional, safety-compliant damage report, utilizing professional roofing replacement services ensures that trained experts inspect your system, document hidden structural failures, and represent your interests during adjuster walk-throughs.

Frequently Asked Questions

How long after a storm do I have to file a roof damage insurance claim?

Most standard homeowner insurance policies require you to file a claim within 12 months of the storm event. However, some insurance carriers require notice within 60 to 90 days. Checking your policy terms and documenting damage immediately after the storm is critical.

Will filing a storm damage roof claim increase my insurance rates?

Storm damage is classified as an "Act of Nature." Unlike an auto accident where you are at fault, insurance companies generally cannot raise your individual rate for filing an Act of Nature claim. However, rates across your entire geographic zip code may rise after a major regional weather event.

What if the insurance adjuster denies my storm damage claim?

If your claim is underpaid or denied, you have the right to request a second inspection with a different adjuster. You can also hire an independent public adjuster or partner with a licensed roofing contractor who can provide a detailed line-item estimate (using industry-standard software like Xactimate) to dispute the denial.

How do services like Mr. Remodel assist during the storm recovery process?

Services like Mr. Remodel connect homeowners directly with vetted, licensed roofing contractors who specialize in storm damage restoration. These professionals assist with thorough roof inspections, detailed insurance documentation, and high-quality system installations.

Should I sign an agreement with a contractor before my insurance claim is approved?

Never sign a binding contract that demands full payment upfront before claim approval. However, signing a standard "Contingency Agreement" with a reputable local contractor is common. This allows the contractor to inspect your roof, meet with your adjuster, and negotiate the scope of work on your behalf, with the contract taking effect only if the insurance company approves the claim.

Secure Your Home's Roof Replacement Today

Documenting storm damage promptly and systematically is the single most important step you can take to protect your home and ensure your insurance claim is paid in full. Don't let unaddressed shingle damage lead to costly leaks or interior rot.

Ready to restore your roof? Reach out to Mr. Remodel to get a free, no-obligation quote and connect with top-rated local roofing specialists who will guide you through every step of the insurance claim process.