Table of Contents [hide]

Who This Is For:

This guide is for homeowners currently facing roof damage or nearing the end of their roof’s lifespan. It helps those weighing the financial impact of insurance claims against the long-term benefits of direct investment.

Key Takeaways

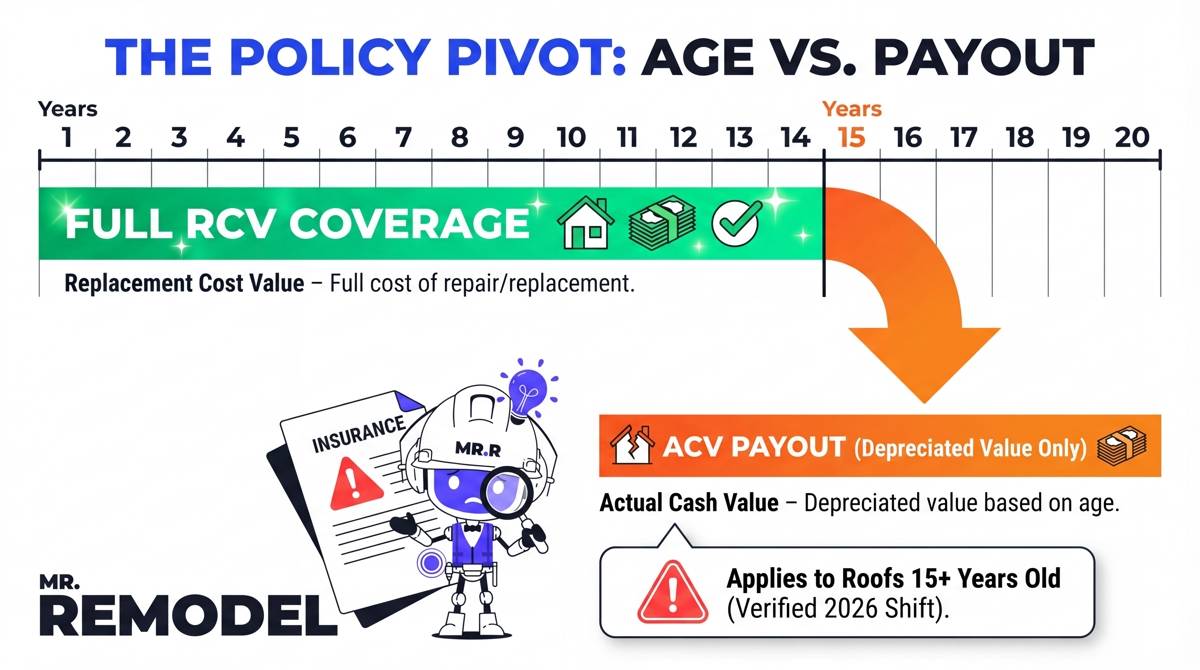

- Policy Shift: This year, most insurers will move roofs over 15 years old to Actual Cash Value (ACV) policies, significantly lowering payouts.

- The $1,000 Rule: If repairs cost less than your deductible, avoid filing a claim to prevent future premium hikes.

- Cost Reality: Standard out-of-pocket replacements range from $7,000 to over $15,000, while a claim often costs only your deductible plus upgrades.

- Regional Trends: Areas like Utah and Pennsylvania see the highest finalized customer capital investments for premium roofing systems.

Deciding how to fund a new roof is one of the most significant financial choices a homeowner will face. According to data from the Insurance Information Institute, the age and condition of your roof are the primary factors in determining your home’s insurability.

For many, the choice between filing an insurance claim or paying out-of-pocket is not just about the immediate cost. It involves understanding complex policy shifts and local market trends. At Mr. Remodel, we see homeowners navigating these hurdles every day as they seek to protect their largest asset.

Understanding the Difference: Insurance vs. Out-of-Pocket

Choosing between these two paths depends on the cause of the damage and your specific policy language. Insurance is designed for sudden and accidental events, while out-of-pocket payments cover maintenance and upgrades.

How Insurance Payouts Work

Insurance coverage generally falls into two categories: Replacement Cost Value (RCV) and Actual Cash Value (ACV). In 2026, there is a major industry shift. Many carriers now move roofs 15 years or older strictly to ACV policies.

This means the insurer subtracts depreciation from your payout. If you have an old roof, you might only receive a fraction of the total replacement cost. This pushes a larger financial burden onto the homeowner, even with a valid claim.

The True Cost of Paying Out-of-Pocket

When you pay out-of-pocket, you have total control over the materials and the contractor. According to Mr. Remodel's data, standard out-of-pocket replacements for asphalt or composite shingles typically range from $7,000 to $15,000 or more.

While this is a larger upfront investment, it avoids the risk of insurance premium increases. It also allows you to choose high-performance materials that may not be covered by a standard insurance "like-for-like" replacement clause.

When to File an Insurance Claim for a Roof

Filing a claim is appropriate when the damage is covered by your policy and exceeds your deductible by a significant margin. Understanding the nuances of your coverage is essential to avoid a denied claim.

Sudden and Accidental Damage

Homeowners' insurance is meant to protect you from unexpected events. The Maryland Insurance Administration specifies that policies typically cover "sudden and accidental" damage.

This includes events like fire, falling trees, or severe storms. If a windstorm rips shingles off your roof, this is usually a clear-cut case for a claim. However, damage caused by a lack of maintenance is rarely covered.

Identifying Storm and Hail Damage

Hail is one of the most common reasons for insurance claims. Even if you cannot see the damage from the ground, hail can bruise the shingles and lead to leaks.

See Related: Storm Damage: Repair or Replace Decision Guide

In states like Colorado, frequent hailstorms make insurance settlements a primary way homeowners fund replacements. However, you must file within the timeframe specified in your policy to ensure the claim is honored.

When Paying Out-of-Pocket Makes More Sense

Sometimes, filing a claim can actually cost you more in the long run. You must weigh the immediate payout against the potential for higher insurance rates or future uninsurability.

Small Repairs vs. Your Deductible

You should strictly follow the math when it comes to minor damage. If a local contractor quotes you $800 for a minor repair but your insurance deductible is $1,000, filing a claim is a mistake.

You would receive $0 from the insurance company while still having a claim on your record. This can lead to inflated premiums for years.

See Related: Roof Leak Repair vs Full Replacement Cost

Normal Wear and Tear Exclusions

Insurance does not cover a roof that has reached the end of its natural life. If your roof is 25 years old and simply wearing out, your insurer will likely deny the claim.

In these cases, paying out-of-pocket is your only option. Investing in a full replacement now can prevent interior water damage that would be even more expensive to fix later.

See Related: Roof Repair vs Replacement: Cost, Lifespan & Decision Guide

ACV vs. RCV: Why Policy Type Matters

The type of policy you hold dictates your out-of-pocket responsibility during a claim. The Texas Department of Insurance emphasizes that homeowners must understand these definitions before disaster strikes.

Actual Cash Value (ACV) and Depreciation

Under an ACV policy, the insurer pays what the roof is worth at its current age. If a 20-year-old roof is damaged, the insurance company will deduct 20 years of "wear and tear" from the payout.

For many homeowners in 2026, this results in a check that covers less than 50% of the actual replacement cost. You will have to cover the remainder out-of-pocket.

Replacement Cost Value (RCV) Benefits

An RCV policy is more comprehensive. It covers the cost to replace the roof with a new one of similar quality, regardless of the old roof’s age.

While you still have to pay your deductible, the insurance company covers the rest of the bill. This makes RCV policies much more valuable, though they often come with higher monthly premiums.

Regional Cost Data and Local Investments

Roofing costs vary significantly based on location, climate, and local labor rates. Mr. Remodel data tracks finalized customer capital investments to show what homeowners are actually spending across the country.

|

|

These numbers reflect the total amount invested by customers to ensure their homes are fully protected. In Florida, for example, the investment is often focused on meeting strict wind-resistance codes following hurricane seasons.

Maximizing Your Investment with a Trusted Contractor

Whether you are using insurance funds or your own savings, the quality of the installation is what determines the lifespan of your roof. Hiring expert roofing and exterior professionals ensures that the job is done to code.

Managing the Claims Process

If you choose to file a claim, having a contractor present during the adjuster's inspection is helpful. They can point out damage the adjuster might miss, such as hidden flashing issues or deck rot.

Investing in Longevity

If you are paying out-of-pocket, consider materials that offer better durability. While the upfront cost is higher, a roof that lasts 40 years is a better value than one that needs replacing in 15 years.

See Related: How Long Do Roofs Last? Lifespan by Material & Climate

Before you commit to a major expenditure, it is wise to get a free quote on your roof replacement to understand your specific local costs.

Frequently Asked Questions

Does insurance cover a 20-year-old roof?

It depends on the policy and the cause of damage. In 2026, many insurers will move roofs of this age to ACV policies, meaning they will only pay the depreciated value. Maintenance issues are never covered.

Will my insurance premiums go up if I file a roof claim?

Often, yes. While some states have laws preventing hikes for "Acts of God," many carriers will increase rates or remove "no-claim" discounts after a filing.

What is a wind deductible?

Common in states like Florida, this is a separate, often higher deductible specifically for damage caused by wind or hurricanes. It is usually calculated as a percentage of your home’s insured value.

How can Mr. Remodel help with my roof replacement?

Services like Mr. Remodel help by matching you with vetted, local contractors who understand both insurance work and out-of-pocket installations. This ensures you get an accurate quote and professional service.

Is it better to pay out-of-pocket even if I have insurance?

If the damage is minor or if you want to avoid a claim on your record, paying out-of-pocket is often smarter. It also gives you more flexibility to choose premium materials that insurance might not cover.

Choose the Best Path for Your Roof Replacement

Deciding between an insurance claim and an out-of-pocket payment requires a careful look at your policy and the extent of the damage. For major storm damage, insurance provides a necessary safety net. For aging roofs or minor repairs, paying directly often preserves your insurability and long-term savings.

No matter which path you choose, Mr. Remodel is here to simplify the process. We connect you with top-rated local professionals and provide free, no-obligation quotes to help you make an informed decision.

Ready to protect your home? Get a free, no-obligation quote and connect with the best roofing contractors in your area.