Table of Contents [hide]

Who This Is For

This authoritative guide is built for homeowners currently facing a residential water crisis. It provides step-by-step instructions for mitigating damage, documenting losses, and navigating complex insurance adjusters. If you need fast claim approval and immediate structural protection, this resource provides the exact roadmap.

Key Takeaways

- Immediate Action is Mandatory: Standard homeowners policies require you to mitigate damage immediately to prevent secondary issues.

- Coverage Depends on the Source: Sudden and accidental pipe bursts are typically covered, while gradual leaks and ground floods are heavily scrutinized or denied.

- Documentation Drives Approvals: Professional moisture mapping and daily photographic logs are the single biggest factors in rapid claim resolution.

- Regional Climates Alter Claims: Your location dictates your primary risks, from California atmospheric rivers to New York winter freezes.

- Q4 Brings Peak Vulnerability: Historical data reveals a massive spike in water damage incidents during October and November.

- Phone Calls Beat Web Forms: During a crisis, immediate verbal dispatch secures faster professional intervention than waiting for email replies.

- Mold is Often Excluded: Failing to dry a property within 48 hours introduces mold, a secondary risk that many standard policies strictly limit or deny.

Water damage is one of the most common and financially devastating events a property owner can face. It strikes without warning and immediately begins degrading the structural integrity of your home. The longer water sits, the more expensive the recovery becomes.

According to internal market data from Mr. Remodel, 100% of emergency water mitigation requests originate from urgent phone calls. Homeowners in crisis do not have the luxury of filling out web forms and waiting for business hours. They need immediate, localized intervention.

Understanding how to position your insurance claim in the first 24 hours is critical. A single misstep in documentation or a delayed response can result in thousands of dollars of denied coverage. You must approach this process with precision.

The Zero-Minute Response Checklist

When water breaches your living space, panic is a natural reaction. However, insurance providers require you to act rationally and fulfill your legal duty to mitigate further damage. Faltering here can jeopardize your entire financial recovery.

The first step is completely severing the water supply to the property. Locate your primary water shutoff valve and turn it clockwise until the flow stops. If the water source is a localized appliance, close the supply valve directly behind it.

Next, prioritize electrical safety above all else. If water is approaching wall outlets or submerged electrical appliances, do not enter the room. Disconnect the main power breaker to the affected zone immediately to prevent lethal electrical hazards.

Once the area is safe, begin moving high-value portable items out of the wet zone. Elevate furniture on foam blocks or aluminum foil to prevent wood stains from bleeding into wet carpets. This demonstrates to your adjuster that you actively protected your personal property.

See Related: What To Do Immediately After Water Damage

Decoding Your Homeowners Insurance Policy

Insurance policies are notoriously complex contracts filled with legal jargon. To successfully secure an approval, you must understand the exact language your provider uses to define covered perils. Misunderstanding these terms is the leading cause of denied claims.

According to the Insurance Information Institute, standard homeowners insurance typically covers water damage if the cause is sudden and accidental. A frozen pipe bursting in the middle of the night perfectly fits this definition.

Coverage A: Dwelling Protection

Dwelling coverage applies to the physical structure of your home. This includes the framing, drywall, built-in cabinetry, and hardwood flooring. If a covered peril damages these elements, Coverage A pays for the tear-out and reconstruction.

Coverage B: Personal Property

Personal property coverage protects your movable belongings. Furniture, electronics, and clothing ruined by a sudden pipe burst fall under this category. Adjusters will calculate the actual cash value or replacement cost depending on your specific policy terms.

Coverage C: Loss of Use

If your home becomes uninhabitable due to severe structural water damage, Coverage D activates. This section covers additional living expenses. It pays for hotel stays, restaurant meals, and temporary housing while your property undergoes extensive mitigation and reconstruction.

The Maintenance Exclusion Clause

Insurance companies expect homeowners to maintain their properties. If an adjuster discovers that a roof has been leaking for six months due to missing shingles, they will classify the damage as a maintenance failure. Gradual damage is almost universally excluded from coverage.

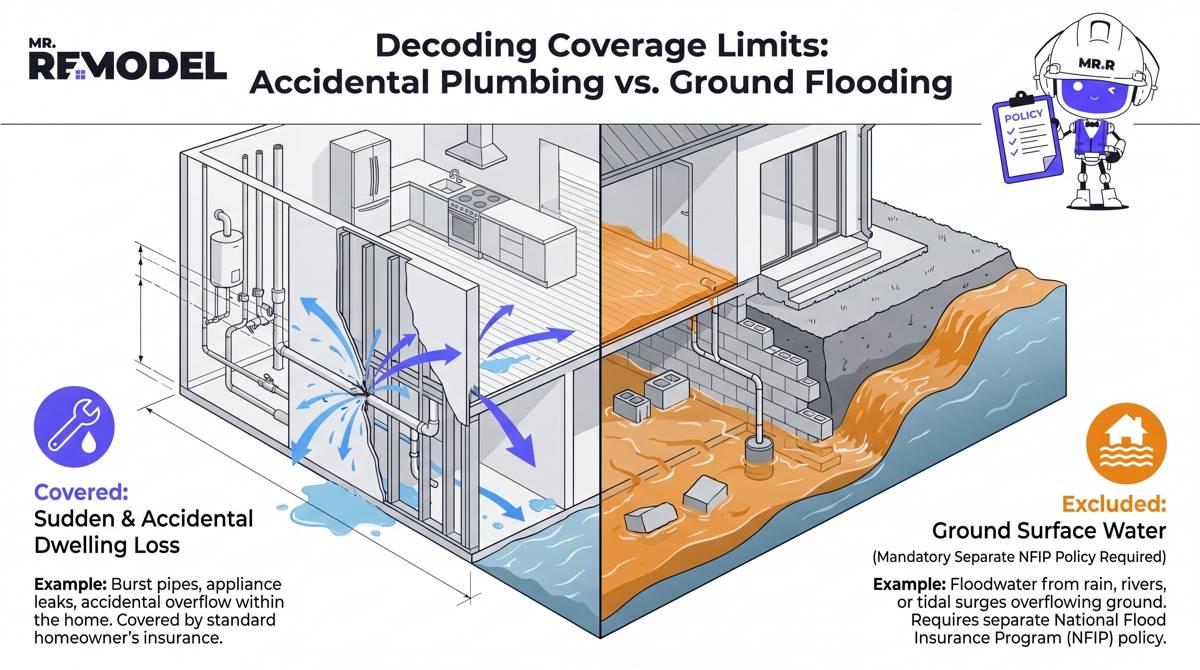

The Flood Discrepancy: Standard vs. NFIP Policies

One of the most devastating discoveries a homeowner can make is learning their standard policy does not cover natural flooding. The insurance industry strictly defines what constitutes a flood, and it differs vastly from internal plumbing failures.

A flood is defined as a general and temporary condition of partial or complete inundation of two or more acres of normally dry land. It also applies if two or more properties are affected by rising surface waters. Standard policies do not cover this.

To protect against rising rivers, storm surges, or heavy rainfall inundation, you need a separate policy. The Federal Emergency Management Agency manages the National Flood Insurance Program. Homeowners in high-risk zones must carry this distinct coverage to survive coastal or riverbed disasters.

Table 1: Claim Types and Likely Coverage Outcomes

|

|

Regional Infrastructure Vulnerabilities

Water damage risks change dramatically depending on your geographical location. Local climates and aging municipal infrastructures create highly specific threats. Insurance providers assess claims differently based on these known regional hazards.

Mr. Remodel data indicates a massive 60.58% volume spike in emergency water events during the fourth quarter. As October and November arrive, rapid temperature shifts and severe seasonal storms test the limits of residential building envelopes nationwide.

California: Atmospheric Rivers and Aging Plumbing

California faces unique challenges driven by sudden atmospheric rivers dumping massive volumes of rain in hours. When combined with the aging galvanized plumbing found in mid-century coastal homes, the risk of both exterior intrusion and interior pipe failure skyrockets.

Insurance claims in California frequently battle over the definition of wind-driven rain versus rising surface water. Property owners must document exactly how water entered the structure to ensure the claim falls under standard dwelling coverage rather than excluded flood scenarios.

Florida: Storm Surges and Hurricane Force Winds

Florida properties endure intense humidity and devastating hurricane seasons. Water damage here is often catastrophic, involving entire ground floors submerged in Category 3 black water. Standard policies frequently push these claims to separate windstorm or flood deductibles.

Florida homeowners face aggressive timelines. The extreme heat accelerates material degradation and bacterial growth. Mitigation teams must deploy industrial desiccant dehumidifiers immediately to save structural framing from total rot.

New York: Extreme Freeze and Thaw Cycles

In New York, the primary threat emerges during brutal winter cold snaps. Poorly insulated exterior walls allow temperatures to plummet around copper supply lines. The water inside freezes, expands, and shatters the pipe walls.

When the temperature thaws, hundreds of gallons of water spray unseen into wall cavities. New York adjusters look closely for proof that the homeowner maintained adequate indoor heating. If a property was left unheated during a freeze, the resulting burst pipe claim will face heavy scrutiny.

Table 2: Regional Risk Profiles and Claim Challenges

See Related: Insurance Coverage for Water Damage

Professional Documentation Strategy

The gap between a denied claim and an instant approval lies entirely in documentation. Adjusters are trained to minimize payouts where evidence is lacking. You must provide an overwhelming, undeniable visual record of the disaster.

Do not begin cleaning or throwing away ruined materials immediately. Take wide-angle photographs of every affected room to establish the overall scale of the flooding. Follow this with close-up shots of the specific water source, such as the ruptured valve or shattered pipe.

Record a continuous video walking through the property. Narrate the video, detailing the time, date, and exact depth of the standing water. Open cabinet doors and closet spaces on camera to show hidden moisture migration.

Keep a precise, written log of every action you take. Note the exact time you shut off the main water valve. Save all receipts for emergency plumbing hardware, wet vac rentals, or hotel stays. This paper trail forces the insurance company to reimburse your immediate out-of-pocket mitigation costs.

Hiring the Right Restoration Contractor

Attempting a DIY dry-out on a major structural flood is a guaranteed way to ruin your property value. Standard household fans cannot pull deep moisture out of hardwood floors or dense drywall. You must bridge the gap between amateur cleaning and certified professional mitigation.

Insurance companies respect data. When you hire a certified mitigation firm, they arrive with thermal imaging cameras and psychrometric sensors. They generate daily moisture logs that prove mathematically that your home requires professional intervention.

This level of professional documentation removes the adjuster's ability to argue against the severity of the damage. Ensure the contractor you choose utilizes industry-standard estimating software. This guarantees their line-item pricing aligns with your insurance provider's approved cost databases.

See Related: Questions To Ask a Water Damage Contractor

Stop fighting your insurance adjuster alone. Connect with platforms like Mr. Remodel right now. Instantly connect with certified local contractors who speak the insurance industry's language and fight for your maximum claim approval.

The Secondary Menace of Microbial Mold

Water damage is a race against time. If porous materials remain wet for more than 48 hours, microbial growth becomes inevitable. Mold poses severe respiratory risks and creates an entirely new layer of insurance complications.

According to the Environmental Protection Agency, controlling indoor moisture is the only effective way to prevent mold growth. Standard cleaning supplies cannot penetrate drywall paper to kill hidden spores. Professional antimicrobial treatments are mandatory.

Many modern insurance policies contain strict mold limitations or outright exclusions. If your adjuster determines that mold grew because you delayed emergency extraction, they will deny the mold remediation portion of the claim. This leaves you paying thousands out of pocket for biohazard cleanup.

Rapid, documented water extraction is your best defense against mold exclusions. By proving you hired professionals on day one, you shift the liability away from homeowner neglect and preserve your maximum policy limits.

Table 3: Timeline of a Typical Water Damage Claim

The Q4 Preparedness Protocol

Historical data proves that October and November represent a critical danger zone for homeowners. The 60.58% volume spike in emergencies during this period is entirely predictable. Proactive homeowners must prepare their properties before the first major weather event hits.

Start by inspecting your exterior envelope. Clean all gutters and downspouts to ensure heavy autumn rains route safely away from your foundation. Disconnect all exterior garden hoses to prevent residual water from freezing and cracking the interior spigot pipes.

Insulate vulnerable plumbing in crawlspaces, basements, and attics. Wrapping exposed pipes in foam insulation sleeves costs very little but provides massive protection against deep freezes. Finally, test your main water shutoff valve to ensure it turns smoothly during a true panic scenario.

Post-Claim Recovery and Rebuilding

Once the mitigation phase concludes and your property is certified dry, the rebuilding phase begins. This is a highly specialized construction process. Replacing flood-cut drywall, matching existing textures, and installing new flooring requires skilled tradesmen.

Do not accept the first settlement check if it seems too low. Insurance companies often send an initial actual cash value payment that deducts depreciation. Once the repairs are complete, you can submit the final invoices to claim your recoverable depreciation and cover the total replacement cost.

Use this reconstruction period as an opportunity to upgrade your home's resilience. Instead of installing standard drywall in a basement, opt for moisture-resistant green board. Replace moisture-sensitive laminate with waterproof luxury vinyl plank flooring to minimize future risks.

See Related: How To Prevent Future Water Damage

Comprehensive FAQ Section

What is the very first thing I should do when I discover water damage?

Immediately shut off the main water valve to stop the source of the flooding. Next, disconnect electrical power to the affected areas to prevent shock hazards, and begin taking wide-angle photographs of the damage for your insurance claim.

Will my standard homeowners insurance cover a flooded basement?

It depends entirely on the source of the water. If the flood was caused by a sudden indoor pipe burst, it is typically covered. If the flood was caused by ground surface water or rising rivers, standard policies will deny the claim without a separate NFIP flood policy.

How do I prove to the adjuster that the damage was sudden and accidental?

You must provide immediate photographic evidence and professional moisture mapping logs. Hiring a certified mitigation team on the first day demonstrates that the event was sudden and that you fulfilled your duty to mitigate further damage.

What is a public adjuster, and do I need one?

A public adjuster is a licensed professional you can hire to represent your financial interests during a complex claim. While independent adjusters work for the insurance company, public adjusters work for you, though they take a percentage of your final settlement as their fee.

How does Mr. Remodel help me with my water damage claim?

Mr. Remodel connects you with highly vetted local extraction specialists. These professionals utilize industry-standard estimating software and provide the exact moisture data your insurance adjuster needs to approve your claim instantly.

Are the contractors provided by Mr. Remodel certified to handle mold?

Yes. The restoration experts within the Mr. Remodel network carry specialized certifications in structural drying and microbial remediation. They deploy commercial-grade antimicrobial treatments to ensure your home is safe and compliant with health standards before rebuilding begins.

Why did my insurance company deny my claim for a leaking shower pan?

Insurance policies typically exclude damage resulting from long-term wear and tear or poor maintenance. A leaking shower pan usually degrades over months or years, which adjusters classify as gradual damage rather than a sudden, covered peril.

How long does the structural drying process usually take?

With professional industrial equipment, standard residential drying takes between three and five days. However, severe Category 3 black water incidents or dense materials like hardwood flooring may require specialized desiccant drying that extends the timeline up to a week.

Secure Your Financial Recovery Today

Navigating a water damage insurance claim requires speed, precise documentation, and professional validation. Do not let complex insurance jargon or intimidating adjusters prevent you from recovering your home's true value. By taking immediate action and partnering with certified experts, you guarantee your property is restored safely and correctly.

Stop guessing and start rebuilding. Get in touch with Mr. Remodel and connect with local contractors who will secure your property, document your losses, and fight for the comprehensive insurance approval you deserve. Get your free, no-obligation quote to start your water damage restoration project.