Table of Contents [hide]

Who This Is For:

This guide is designed for homeowners planning a roof replacement who want to maximize their return on investment. It is especially helpful for those in high-risk weather zones, such as Florida or Texas, looking to lower annual insurance premiums through strategic material upgrades.

Key Takeaways

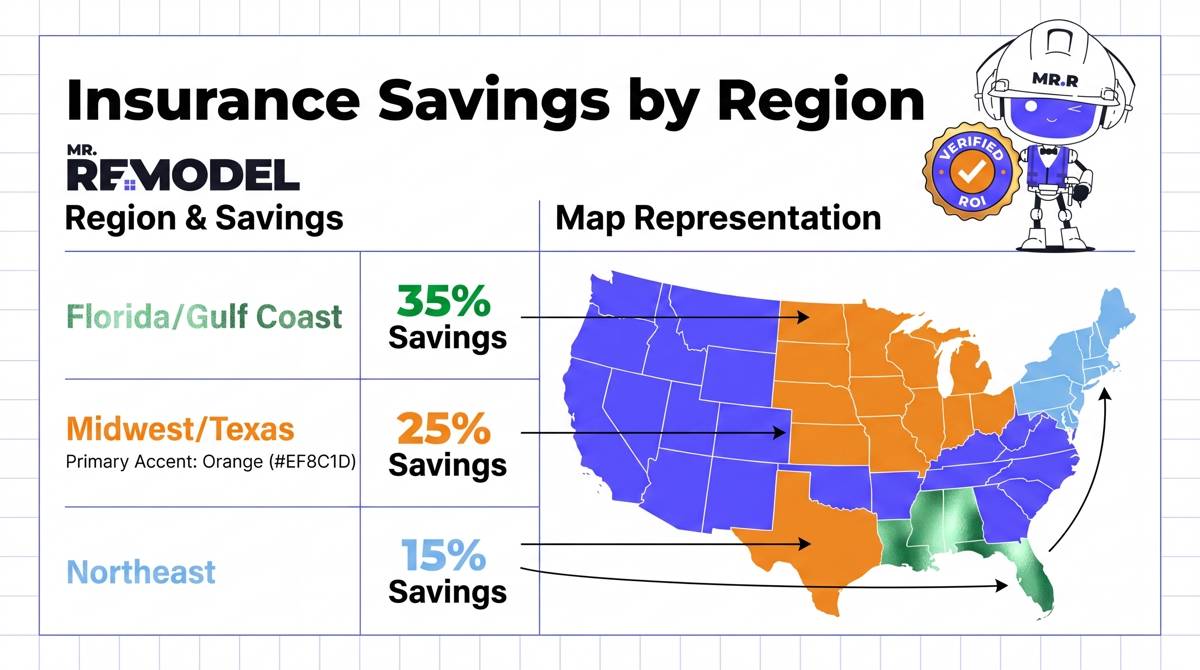

- Significant Savings: A new roof can reduce your homeowners' insurance premiums by 5% to 35%, depending on your location and material choice.

- Safety Standards: Materials with a UL 2218 Class 4 impact-resistance rating offer the most substantial and consistent insurance discounts.

- Automatic Updates Do Not Exist: Insurance companies rarely update your roof’s age in their system automatically. You must proactively submit documentation to trigger a rate review.

- Risk Mitigation: Upgrading from old 3-tab shingles to architectural shingles or metal reduces the likelihood of leaks, which insurers reward with lower rates.

Replacing a roof is one of the most significant investments a homeowner will ever make. The national average cost for a roof replacement currently sits at $25,307.08, according to Mr. Remodel data. While the upfront price is high, the long-term financial benefits extend far beyond simple curb appeal.

One of the most immediate ways to recoup this cost is through your homeowners' insurance policy. Because a new roof is the primary defense against water damage, insurers view it as a massive reduction in risk. In many cases, an aging roof is a liability that can lead to policy cancellation if not addressed.

The Financial Impact of a New Roof on Your Policy

When you install a new roof, you are essentially hardening your home against the elements. Insurance providers calculate your premium based on the likelihood of a future claim. A roof that is 20 years old is statistically much more likely to fail than one installed this year.

How Much Can You Actually Save?

Most homeowners see a premium reduction between 5% and 20% after a professional installation. However, in states prone to severe weather, these savings can climb as high as 35%. This reduction is often categorized as a "new roof discount" or a "wind mitigation credit."

The Importance of Roof Age

Insurers often shift how they pay out claims based on the age of your roof. For roofs over 20 years old, many companies transition from Replacement Cost Value (RCV) to Actual Cash Value (ACV). According to the Insurance Information Institute, this means they only pay the depreciated value of the roof during a claim.

See Related: How Long Do Roofs Last? Lifespan by Material & Climate

How Roof Materials Influence Insurance Costs

The material you choose has a direct correlation to the discount you receive. While standard architectural shingles are popular, they do not always trigger the highest tier of savings. Insurers look for specific certifications that prove the material can withstand hail and high winds.

Asphalt Shingles vs. Metal Roofing

Standard architectural shingles average around $25,389.92 for a full replacement. These provide a solid baseline for insurance discounts. However, metal roofing is rapidly growing in popularity. Currently, 18.9% of Mr. Remodel leads specifically request metal options for their durability and superior protection.

The Power of UL 2218 Class 4 Ratings

To get the best possible discount, look for materials with a UL 2218 Class 4 rating. This is the industry gold standard for impact resistance. The International Institute of Building Enclosure Consultants notes that Class 4 materials can withstand the impact of a 2-inch steel ball dropped from 20 feet without cracking.

See Related: Roof Replacement ROI by Material Type

Regional Variations in Insurance Savings

Where you live determines how much your insurance agent cares about your roof. In the "Hail Alley" of the Midwest or the hurricane-prone coasts, a new roof is a necessity for maintaining coverage.

High-Cost and High-Risk Markets

In Florida, the average replacement cost jumps to $31,882. In this market, a new roof isn't just about a discount. It is often a requirement to keep your policy active. Texas also sees high lead volumes due to frequent storm activity and the need for wind-mitigation features.

The Texas Department of Insurance highlights that mitigating peril risks through better materials and adjusting deductibles can lead to significant annual savings.

See Related: Insurance Claims vs Out-of-Pocket Roof Replacement

Steps to Claim Your Insurance Discount

Your insurance company will not call you to offer a discount just because they saw a contractor's truck at your house. You must take specific steps to ensure your premiums are adjusted correctly.

1. Request a Wind Mitigation Inspection

In many states, a certified inspector must verify the roof’s features. They will look at the roof-to-wall attachments, the type of nails used, and the water-shedding capabilities. This report is the primary document used to justify a premium drop.

2. Provide the Final Invoice and Permit

Submit your final paid invoice to your insurance agent. This proves the work was completed by a licensed professional. Using professional roof replacement services ensures that all necessary local permits are pulled, which adds another layer of validation for the insurer.

3. Ask for a Full Policy Review

Once the new roof is in the system, ask for a complete review. This is also a good time to compare average replacement costs against your coverage limits to ensure you are not under-insured for the new value of the structure.

Maximizing ROI Through Strategic Replacement

Timing is everything when it comes to ROI. Mr. Remodel data shows that 40.6% of consumers require their projects to start within 7 days. This level of urgency often indicates that a roof has already failed or a claim is pending.

Waiting until a leak occurs can lead to secondary damage, which increases the total cost of ownership. By being proactive, you can select no-leak materials pricing that fits your budget while securing your insurance discount before the next storm season arrives.

See Related: Roof Replacement ROI: Home Value, Insurance & Energy Savings

Understanding the Difference Between Repair and Replacement

Insurers rarely offer discounts for minor repairs. While a patch might stop a leak, it does not change the overall risk profile of the structure. A full replacement is usually required to trigger a change in your premium status.

See Related: Signs You Need a New Roof (vs Repair)

If you are unsure whether your current damage warrants a full claim or just a quick fix, it is best to consult with an expert. Comparing the long-term savings of a new system versus the recurring costs of maintenance is essential for financial planning.

See Related: Roof Leak Repair vs Full Replacement Cost

Frequently Asked Questions

Does a new roof automatically lower insurance?

No, it is not automatic. You must notify your insurance provider and often provide a wind mitigation report or a final invoice to receive the discount.

What is the best roof material for insurance discounts?

Metal roofing and Class 4 impact-resistant asphalt shingles typically qualify for the highest discounts because they are less likely to be damaged by hail or wind.

How much does insurance go down after a new roof?

Most homeowners see a reduction of 5% to 20%, but those in high-risk coastal areas may see savings up to 35%.

Will my insurance cancel me if my roof is too old?

Many insurers will refuse to renew a policy if the roof is older than 20 years. Services like Mr. Remodel help by matching you with vetted contractors to replace your roof before coverage is lost.

Do I need an inspection after the roof is replaced?

Yes, a wind mitigation inspection is often required by insurance companies to verify the specific safety features of the new installation.

Securing Your Investment and Your Savings

A roof replacement is a vital upgrade that protects your home and your bank account. By choosing the right materials and proactively contacting your insurance provider, you can significantly lower your annual premiums and increase your home’s ROI.

Ready to lower your insurance costs with a high-quality roof? Mr. Remodel provides free quotes and connects homeowners to local, vetted contractors who understand the specific requirements for insurance discounts.