Table of Contents [hide]

Who This Is For

This guide is for homeowners in the final stages of the vetting process who are evaluating competing bids. It is specifically designed to help property owners understand why professional credentials are the only thing protecting their home equity and personal savings from catastrophic financial liability.

Key Takeaways

- Financial Risk: Homeowners are personally liable for injuries on uninsured job sites.

- Investment Protection: The average $25,307 project requires a multi-million-dollar insurance shield.

- Warranty Survival: Factory certifications are mandatory to maintain a fifty-year material warranty.

- Structural Compliance: Unlicensed crews often bypass permits and hide structural rot.

- Premium Shift: Over 27% of the market now requires specialized technical certifications.

Hiring a roofer without the proper paperwork is a massive gamble with your home equity. In 2026, the cost of professional materials and insured labor makes choosing a contractor a high-stakes financial decision. You are not just buying shingles: you are buying a shield for your largest financial asset.

At Mr. Remodel, we act as a specialized referral network that filters out high-risk contractors before they ever reach your driveway. We are the data-driven bridge connecting you with pre-vetted professionals.

Managing Financial Risk on Your Property

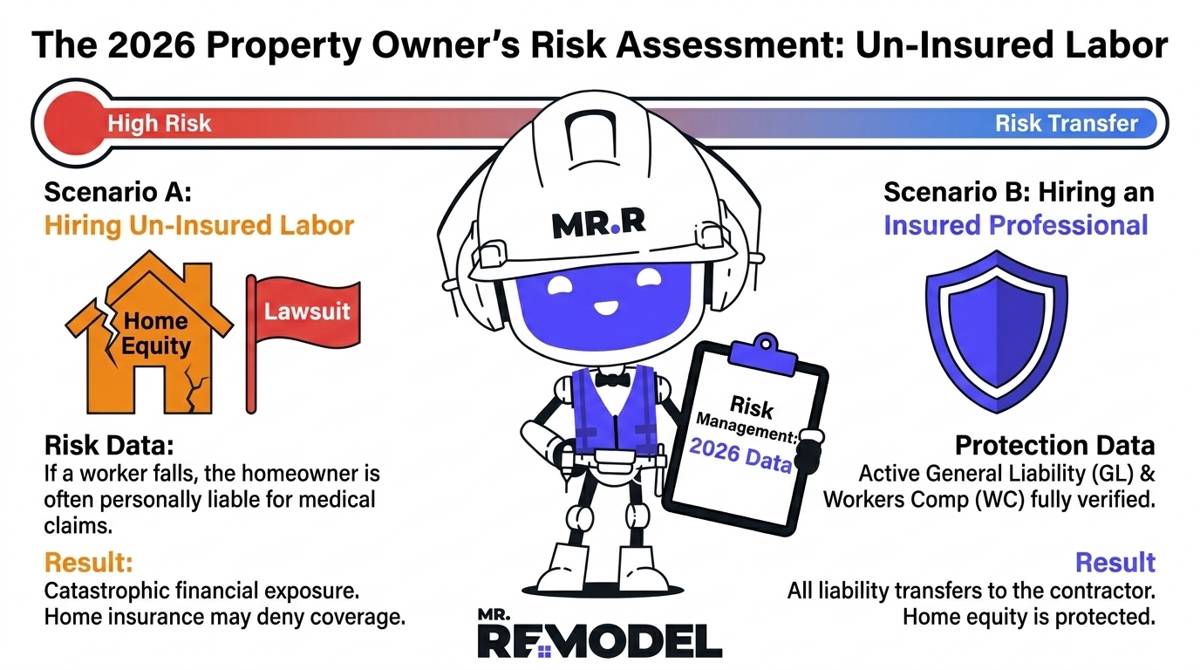

Every time a worker steps onto your property, you assume a level of legal responsibility. Given the average project investment of $25,307.08, the capital at risk is significant. Professional roofing contractor licensing, insurance, and certifications are the only mechanisms that transfer that risk from you back to the professional.

Our data shows that 20% of projects exceed the $30,000 mark due to structural complexities. If an uninsured worker is injured on a high-value job, your personal home insurance may be forced to cover the claim. This can lead to massive premium hikes or even a complete loss of coverage.

See Related: Roof Replacement Cost (2026): Materials, Labor, Regional Pricing & ROI

General Liability and Workers Compensation Coverage

A professional roofing contractor must carry high-limit General Liability (GL) and Workers Compensation (WC) policies. This is a non-negotiable requirement for home protection. In 2025, our network processed project tickets totaling $57,146.10. When a crew is manipulating that much capital, the potential for an accident is real.

The Insurance Information Institute (III) confirms that if a worker falls or property damage occurs on an uninsured site, the homeowner is legally vulnerable. A single spark from a metal cutter could cause catastrophic fire damage to your home. Without professional insurance, you are left paying for these disasters out of your personal savings.

A reputable roofing company should provide proof of these specific insurance protections:

- General Liability coverage with limits of at least $1,000,000 per occurrence.

- Workers' Compensation for every individual present on the job site.

- Professional liability to cover errors in the engineering of the system.

- Umbrella policies that provide extra protection for high-value estates.

See Related: How to Choose a Roofing Contractor: Pricing, Quotes & Red Flags

The Structural Impact of Professional Licensing

Licensing is often viewed as government paperwork, but it is actually proof of competency. A license ensures that the contractor understands modern building codes and the physics of wind uplift resistance. In our latest dataset, 20% of all roofs required structural decking remediation after the tear-off phase.

An unlicensed contractor cannot legally pull municipal permits. This creates a dangerous conflict of interest. If they find rotted wood, they are forced to shingle right over it to avoid a city inspection. This guarantees a structural failure within five years. According to the Federal Trade Commission (FTC), unlicensed contractors are the primary source of bait-and-switch scams.

Why Permits Matter for Your Safety

Municipal permits trigger a third-party review of the contractor's work. This inspection ensures that the installation meets the legal safety standards of your specific region. If a contractor tries to talk you out of a permit, they are likely trying to hide a lack of proper licensing.

Manufacturer Certifications and Warranty Protection

Modern roofing materials are highly technical engineering systems. Over 27% of the market is shifting toward premium materials like metal and slate. This is especially true in states like Montana and West Virginia, where extreme weather is common. These materials require specialized factory-trained certifications.

The Asphalt Roofing Manufacturers Association (ARMA) explains that uncertified installations often void fifty-year warranties immediately. Manufacturers such as Owens Corning or GAF will not honor a material defect claim if the contractor is not factory-certified. You could spend $24,000 on a metal roof only to find you have zero long-term protection.

Certification programs ensure that your contractor follows these factory-required steps:

- Using the correct number of nails for high-wind-resistance zones.

- Installing a complete system of matching starter shingles and ridge vents.

- Utilizing high-grade synthetic underlayment required by the manufacturer.

- Ensuring proper attic ventilation to prevent heat-related shingle blistering.

- Registering your project with the manufacturer for an enhanced warranty.

Before you sign a contract, get a free quote from Mr. Remodel. This ensures you are starting the process with a contractor who is factory-authorized to activate your lifetime warranty.

The Risk of Hiring Discount Roofing Crews

It is tempting to save $5,000 by hiring a crew that operates without these credentials. However, this is a form of financial suicide. You are essentially acting as the general contractor and the primary insurer for a high-risk construction site. One mistake could cost you more than the roof's value.

Premium roofing companies invest thousands of dollars annually in insurance and training. This overhead is what allows them to guarantee their work. When you pay for a premium roofing company, you are paying for the peace of mind that your home and your bank account are fully shielded.

Understanding the 20% Structural Trap

Contractors who lack a license often overlook rotted wood because they lack the technical knowledge to repair it. This is the structural trap. They give you a beautiful surface, but the foundation remains decayed. A licensed professional must pull permits that force them to fix the wood before the shingles go on.

Frequently Asked Questions

How do I verify a contractor's license?

Most states have an online search portal where you can enter a contractor's name or business license number. You should always verify that the license is active and that there are no outstanding legal judgments against the company before you pay a deposit.

What is a Certificate of Insurance?

A Certificate of Insurance (COI) is a document issued by an insurance agency. It lists the types of coverage a contractor has and the effective dates. You should ask the contractor's agent to email this document directly to you. This prevents a contractor from showing you an old or forged document.

Why do manufacturer certifications expire?

Certifications expire to ensure that contractors stay up to date on the latest material changes and building codes. A contractor who was certified ten years ago but has not renewed may not be aware of the current requirements for high-efficiency underlayment or wind-rated fasteners.

Let Us Do the Vetting

The process of calling ten contractors and asking for their insurance papers is exhausting and frustrating. Homeowners often feel pressured into deciding without all the facts. This is where a data-driven filter becomes your greatest asset during a home renovation.

Don't spend hours verifying insurance limits and factory credentials on your own. Submit your project to the Mr. Remodel network. Protect your largest investment and get your free quote today.